Cash Is King

-

November 22, 2017

November 22, 2017

First, cash – or working capital – acts as a safety net if adversity strikes, creating issues with profit and cash flow. If current assets can be turned to cash without disrupting overall operations, you are more flexible – especially in marketing. More specifically, the bushels of stored grain or side pen of cattle can be marketed at a profitable point instead of at a time when cash is most needed to pay expenses, service debt, or payback operating loans.

How One Farmer Benefits from Liquidity

This summer, one young producer indicated he maintains enough working capital to cover up to 40 percent of his total expenses. This includes cash, inventory, receivables, and prepaid expenses minus obligations such as accounts payables, lines of credit, accrued expenses, and principal due within the next 12 months. This strong position allows him to negotiate input costs ranging from land rents to parts and supplies. By maintaining working capital, he is able to capitalize on cash discounts for seed, fertilizer, and feed for his diversified operation. These small discounts added up year after year and ultimately increased his bottom line by just more than 5 percent.

Working Capital Provides Independence

Another benefit of financial liquidity is the negotiation power on capital investments such as machinery, equipment, and land. This position offers two distinct advantages: self-financing and timing. When bargaining with a cash payment, a type of self-insurance is present because no borrowing or additional debt servicing is required.

Additionally, having the cash to make a purchase allows you to quickly and selectively capitalize on deals. For example, some used equipment and breeding livestock are being sold for 60 cents on the dollar for payments in cash, but only for a brief window.

Of course, I am familiar with the long-time argument that cash earns very little sitting in the bank. That is true, but the return from the cash discounts and negotiated deals – when analyzed properly – most often shows a double-digit return in the long-term viability of the business.

On the personal side of finances, I recommend preserving four to eight months (eight to 12 if self-employed) of family living obligations in cash. Of course, the old economic rule is to maintain two months of living expenses in cash. This provides for the unexpected car repair or trip to the emergency room and mitigates the need to rely on expensive credit card debt if adversity strikes.

Rules of Thumb

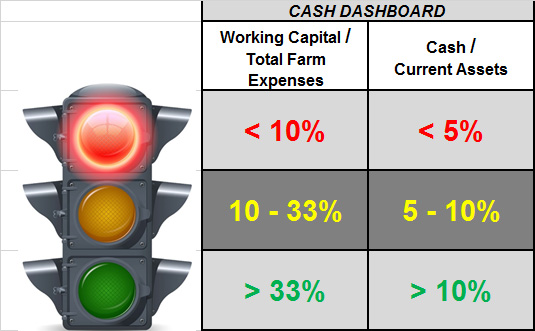

When analyzing your balance sheet, see if you are up to par on financial liquidity by dividing your cash into current assets. You are in a strong financial position if your ratio is between or more than 10 to 20 percent. If you are in the 5 to 10 percent range, caution is warranted as working capital reserves are getting too low. And if you are under 5 percent with credit card debt, accounts payable, or a looming operating line to pay down, you are in a vulnerable and unfavorable position.

Finally, building cash and financial liquidity often entails paying taxes. In many cases, cash or liquid assets are used as a down payment on equipment or other assets to minimize taxes, but over time this builds overhead costs. The prudent producer manages taxes instead of minimizing them. Good managers also balance taxes with cash on hand to navigate the inevitable swings and volatility in global markets.

While perhaps difficult, maintaining cash and operational working capital impacts the bottom line and strategic flexibility. Both the short and long-term advantages of cash negotiations can add to profitability and sustainability. Especially during periods of suppressed prices, increasing available options through flexible liquidity may be the one factor to tip the financial balance in your favor.

How Do You Stack Up?

-

Tag Cloud

patronage liquidity rural marketplace investment Dr David Kohl Essentials Newsletter cash flow scholarships FOMC KOHL-laborations Community Improvement Grants 4-H Education Land Classes Farm Credit College Interest Rates FFA Auction Results Financials employees Land Values balance sheet Focus on Farming calendar appraisals security Weather Outlook land sales farmland auctions